The newsletter for climate-aware risk professionals.

The climate producing today's storms is not the climate that produced the historical record. Join 400+ risk professionals receiving the latest insights from Reask direct to their inbox.

Insights

Unveiling the cracks in the housing market

Rising temperatures and droughts are driving subsidence risk. See how Reask and AXA model climate-linked housing losses across Europe.

Marie Shaylor

|

Senior Research Analyst, IQUW

Mathis Joffrain

|

Natural Hazards Impacts Modeller, AXA

With climate change trends continuing to show increasing temperatures worldwide and with every month of 2024 so far breaking the record as the hottest month globally since records began, many people across all continents will be expecting more extreme weather and scorching temperatures this year.

Increasing temperatures across Europe may pave the way for more prolonged and severe droughts across the continent, and consequently, unfortunate home-owners may begin to feel the calamitous side effects of these as the clay on which their homes are built begins with shrink and swell as the months go by.

How does drought damage homes?

Shrinking and swelling of the sub-surface clays on which some homes are built can lead to a phenomenon called subsidence, where part or all of a homes’ foundation may begin to slowly sink into the Earth. This is a particular problem for homes built on clay minerals; notably, a common foundation soil across much of South England including London.

As a result of a warming climate, Europe is experiencing, in general, milder, warmer winters. One consequence of this is the ability of the atmosphere to hold more moisture, which in turn brings about higher levels of rainfall. During these wetter winter conditions, clay effectively swells up absorbing the extra moisture. This can become a problem in the following Summer season when the clay shrinks as the moisture evaporates over the course of prolonged droughts.

The resulting uneven action of this shrinking and swelling can leave in its wake large structural cracks under the foundations of peoples’ homes, occasionally causing them to buckle under the pressure. Over long periods of time this structural damage can become significant, and make homes unsafe to live in.

There is a growing concern in the insurance industry that an increase in drought activity will lead to an increase in damage and therefore losses caused by subsidence.

“Two-fifths of London’s housing stock, 1.8 million homes, will be susceptible to subsidence by 2030, according to the British Geological Survey.“

—The Economist, Housing and Climate Change, Risk of Subsidence, April 2024

How can we predict subsidence (and how can we protect against it?)

We can use soil water levels from historical reanalyses to calculate a standard measure of soil drought levels known as the Standardised Soil Wetness Index, or SSWI for short. This index represents the changes in soil wetness from the norm on a month-by-month basis when compared to historical levels, allowing us to see when and where severe moisture deficits in soils occur.

We can also measure droughts caused by precipitation (SPI), evaporation (SPEI, ESI), and run-off (SRO) deficits, with these indexes used in addition to SSWI to assess drought impact on other sectors, such as agriculture and industry.

To understand how drought affects the residential sector we focus on soil wetness droughts, since generally considered responsible for the aforementioned shrinking and swelling of clay. Using the example of France, a country which is currently experiencing an uptick in drought subsidence claims, we show how Reask drought data can be leveraged by the insurance industry to predict losses in drought-prone regions.

We look at soil wetness droughts spanning 1, 3 and 6-month time scales and combine them using dimensionality reduction techniques, to get a fuller picture of the severity of droughts over differing time scales. We can then harness climate information from reanalysis products (ERA5) to learn the connection between drought levels and the drivers of drought, using machine learning techniques.

In this way, we can link drought with climate patterns, enabling us to create a climate-dependent stochastic catalogue

We use machine learning combined with climate expertise to learn the relationship between drought levels and climate drivers, based on the historical period (1950 to present).

Once this relationship is learned we can both sample from it to reconstruct a stochastic catalogue of historical drought conditions, and also apply it to future predicted climate model data, enabling us to understand drought risk in a changing climate.

This methodology allows us to recreate, stochastically, both a past and future climatology of drought, ultimately driven by climate predictions and observations.

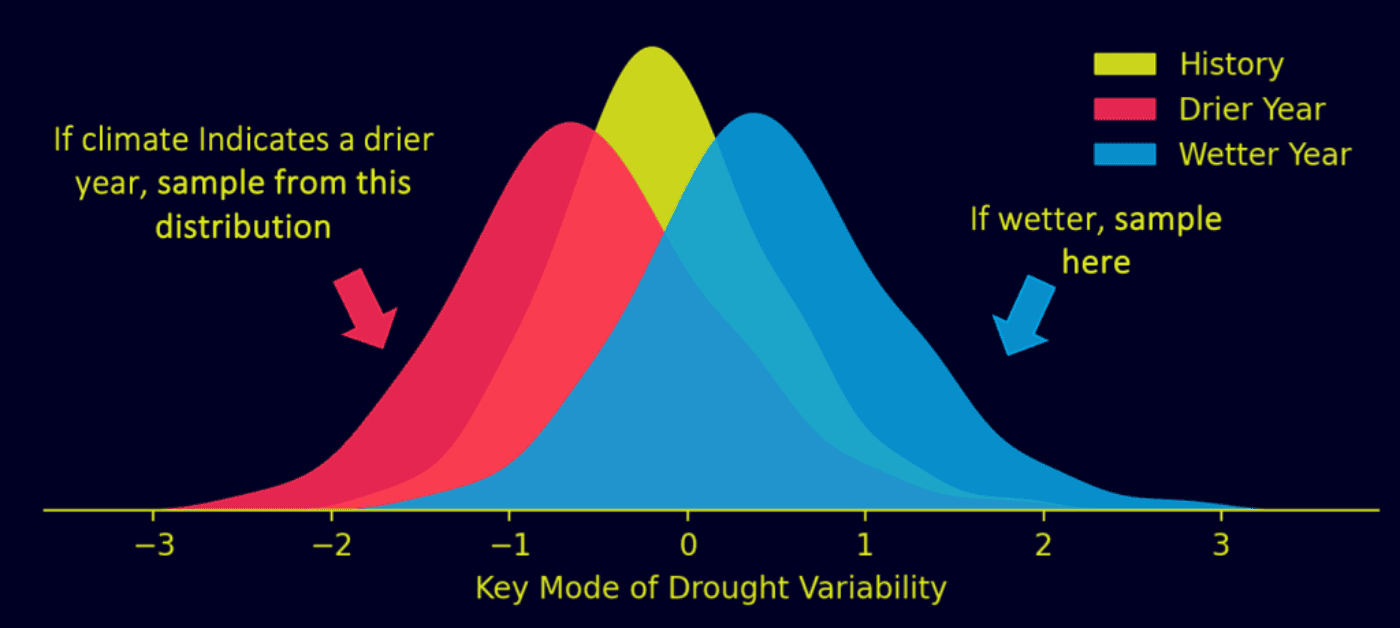

To explain this sampling by way of example, if the climate model we are using says a particular year, say 1995, was very very wet or very very humid, we can sample from a distribution associated with lower drought severities and vice versa.

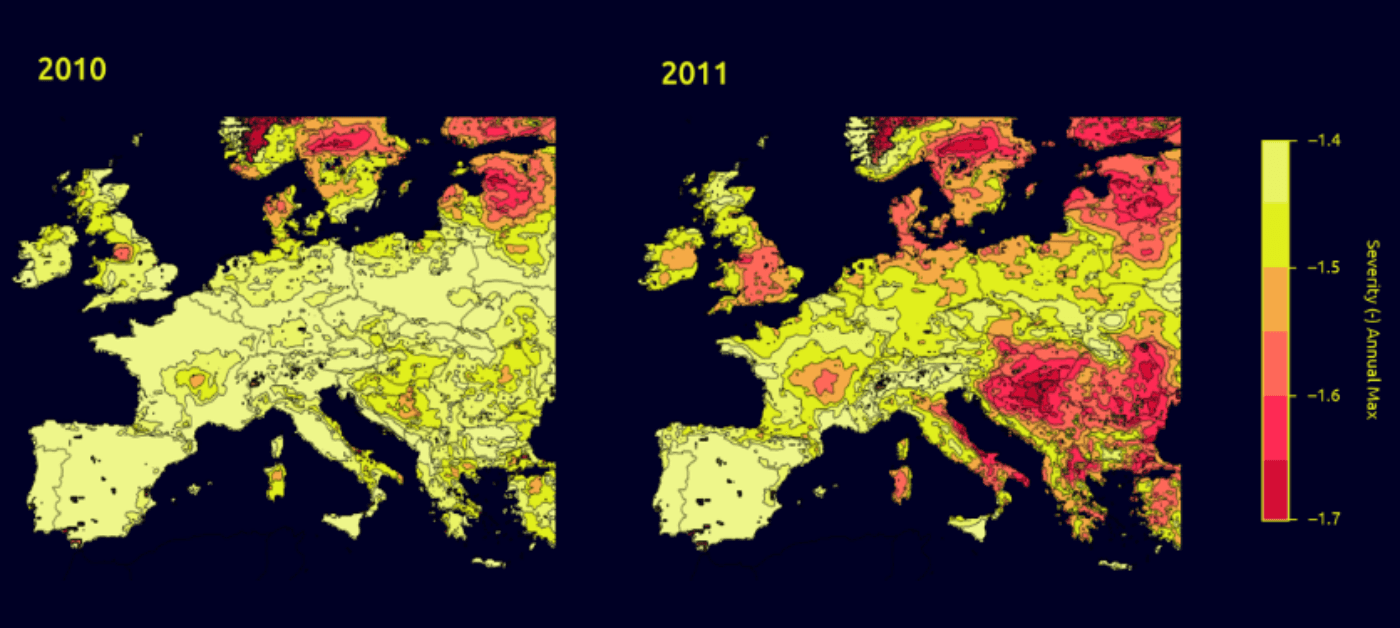

For each year (1950-2100), the distribution is sampled >1200 times to generate over 150,000 stochastic samples for each Reask drought index. The effect of the climate becomes evident when these samples are averaged over each year, as can be seen in the two panels below.

The drought modelling framework also allows for temporal tracking of droughts. As such, we explicitly model the duration, enabling us to separate the effects of short, severe droughts versus more moderate, prolonged droughts.

France: A case in point

Subsidence risk induced by drought has produced material and widespread damage to low-rise buildings in France and insurers expect greater average annual costs in the near future. However, models built to assess this risk are scarce, prompting AXA to partner with Reask to develop an adapted solution. This project brought about three major benefits.

1. Calculating drought-driven loss probabilities with stochastic catalogues

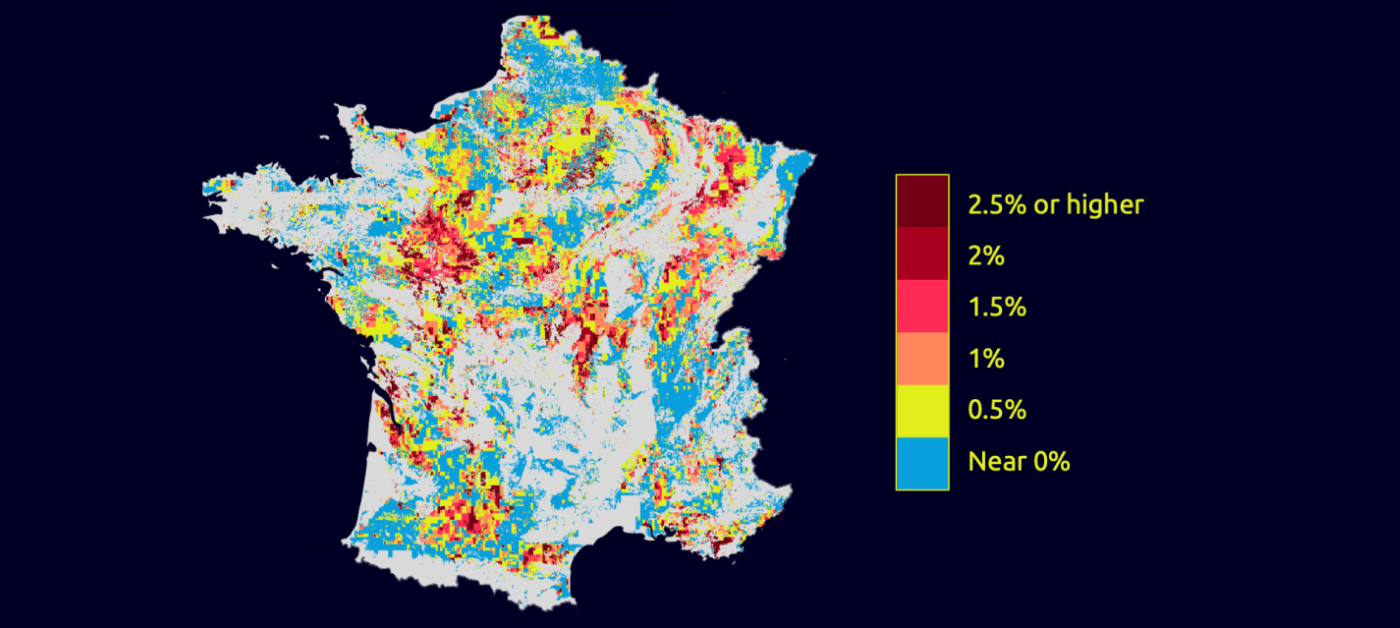

Firstly, the collaboration has allowed AXA to make use of the Reask stochastic catalogues to calculate the full distribution of annual losses over AXA’s exposure at risk. Using the stochastic SSWI index intensity and duration values, soil type data, and combining this with AXA internal exposure data allowed for a direct assessment of claims’ probability per location, based on drought levels.

Using one stochastic sample of an extreme drought event in a given year, the resulting claims probability can be calculated at a high degree of resolution; such as in the example below.

Modelling results show that mean annual losses from drought-induced subsidence are lower yet of a similar order of magnitude as Wind or Flood perils, main risks in France.

These results serve to calculate regulatory quantitative requirements as well as levels of potential risk transfer.

2. Keeping models aligned with new government drought definitions

Secondly, utilising the duration parameter for any given level of dryness makes it possible to adapt the model to the latest drought event definition provided by the French government and therefore, to update the modelling methodology and keep it relevant.

Since May 2024, areas repeatedly subject to moderate drought levels (5-year return period) in the past 5 years are eligible to file an insurance claim.

3. Expanding drought modelling to new sectors and regions

Thirdly, Reask’s extensive range of catalogues makes it possible to extend AXA’s current modelling to business types and geographies. Here, the SSWI index was used to measure drought intensity because it correlates best with AXA subsidence claims, though the wheels are in motion at AXA in undertaking to use other available indices to model impacts such as crop failures or fluvial transport disruptions.

The European scale catalogue enables the replication of the France case study to modelling in the UK, where soil and claims data also exist. Other geographies such as Belgium and the Netherlands may also be the subject of future studies.

With expert insights from guest co-writer Mathis Joffrain

This blog highlights expert insights on drought and loss in climate catastrophes from Mathis Joffrain, a specialist at AXA GRM in France. Mathis has developed and is continuing to develop innovative solutions in affiliation with both the startup sector and academia to assess the economic impacts of natural catastrophes.