Case study

Mar 31, 2026

Improving ILS portfolio returns using seasonal climate forecasts

Ian Bolliger

A 40-year back-test showing how climate-conditioned catastrophe modelling improved ILS portfolio returns by up to 30% and reduced drawdowns by up to 50% in high-loss years.

Research partner | LGT ILS Partners |

Sector | ILS asset management |

Reask models | Reask's Unified Tropical Cyclone (UTC) model and Climate-Based Risk Adjuster (CBRA) |

Use case | Seasonal risk forecasting and ILS portfolio optimization |

Published in | Research Square preprint (peer review in progress) |

Geography | US hurricane exposure (Gulf and Atlantic coasts) |

The challenge: static cat models create a blind spot for ILS portfolio managers

Catastrophe models used across insurance, reinsurance, and capital markets are built around long-term stationary climatologies. They treat historical averages as a reliable guide to current and future risk.

For ILS portfolio managers, this creates a structural blind spot: pricing and capital allocation decisions typically rely on static loss distributions that ignore predictable, year-to-year variations in hurricane activity driven by seasonal weather patterns.

The question we set out to answer was whether seasonal weather information, already well-developed in the forecast community, could be translated into dynamically updated loss distributions that would materially improve portfolio performance. No widely adopted framework existed to do this.

The approach: climate-conditioned catastrophe modelling with CBRA and UTC

Francesco Comola and colleagues at LGT ILS Partners, working with Reask’s Principal Quantitative Engineer, Ian Bolliger and CEO, Jamie Rodney, developed a climate-conditioned catastrophe modelling framework combining two components:

Reask's Unified Tropical Cyclone (UTC) model, which simulates stochastic hurricane seasons conditioned on seasonal ensemble weather forecasts. Specifically, we force UTC with ECMWF’s SEAS5 6-month forecasts initialised each June, producing climate-aware hurricane landfall probabilities along the US coastline. For more about the methodology underpinning this work, see From plausible to useful: hurricane science and risk decision making.

Reask's Climate-Based Risk Adjuster (CBRA), a Python package that adjusts the output of a standard catastrophe model to reflect the expected climate state of each season, modifying event frequency, intensity, and landfall patterns accordingly.

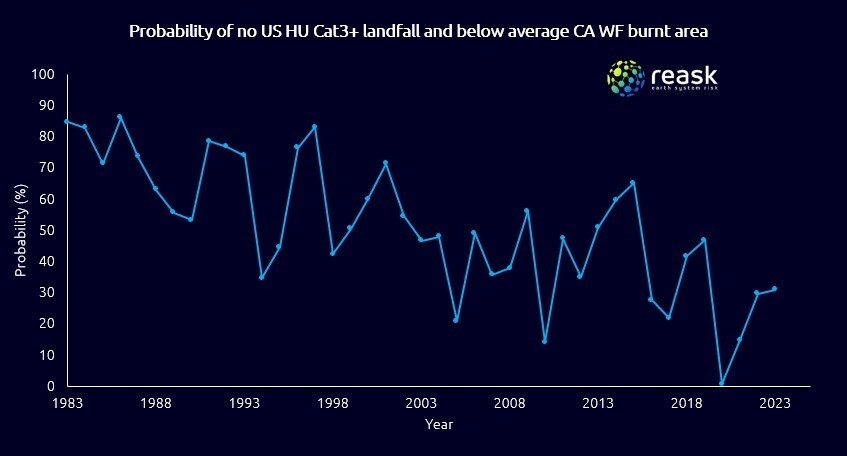

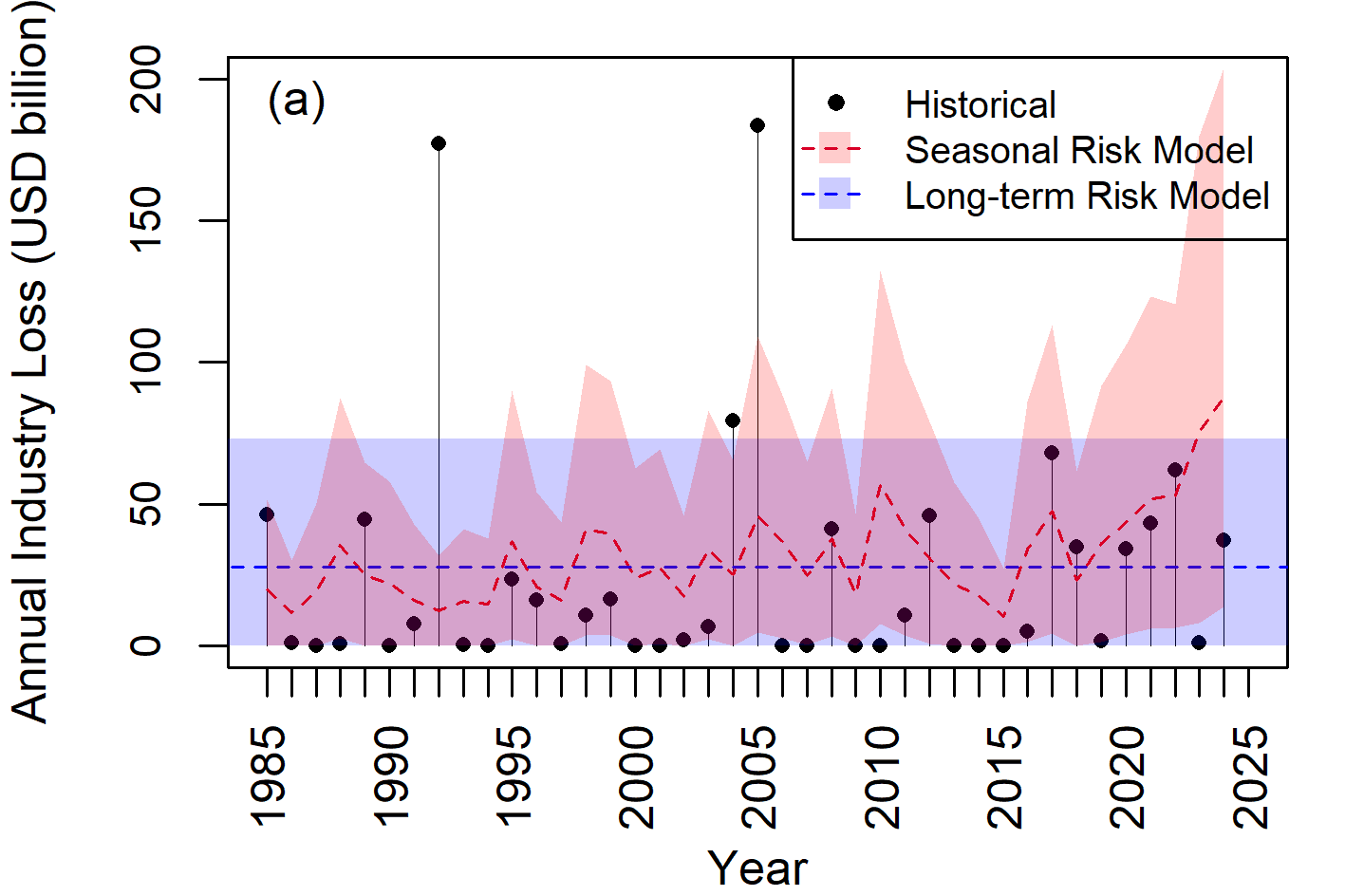

Annual industry losses modelled under static long-term climatology (blue) and the seasonal climate-conditioned model (red), 1985–2024. Source: Figure 1a, Comola et al. (2026).

The team then simulated a systematic investment strategy in a portfolio of 36 regional industry loss warranties (ILWs) over a 40-year period (1985-2024), with annual capital allocations guided by the seasonal climate-conditioned model benchmarked against a static long-term climatology approach.

The analysis used real-world data throughout: stochastic loss tables from a widely used commercial catastrophe model, historical insured hurricane losses from the official US reporting agency (Property Claim Services), and broker-quoted ILW prices.

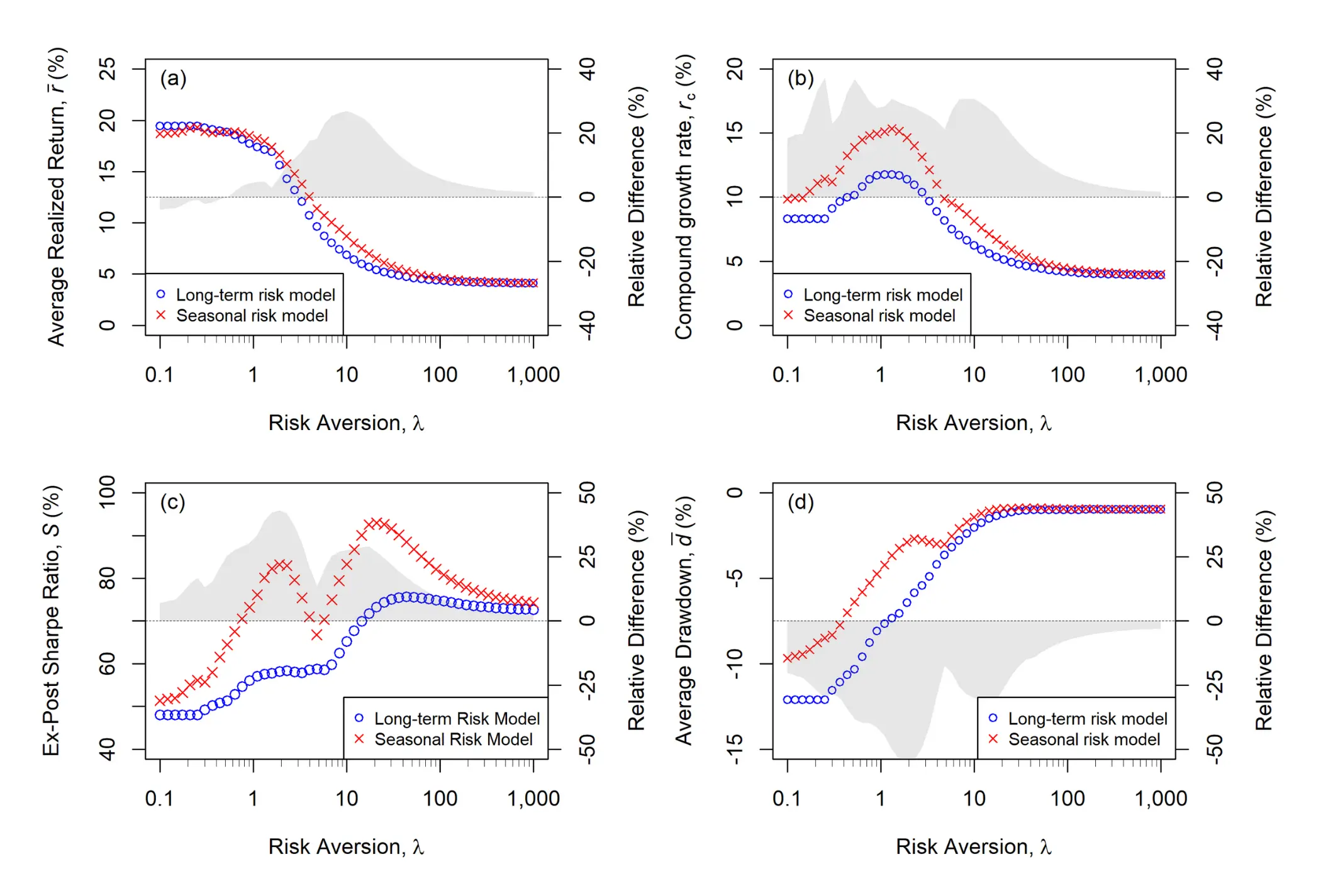

The result: 40-year back-test shows up to 30% higher ILS returns

The climate-conditioned strategy consistently outperformed the static benchmark across the full 40-year evaluation period:

Investment performance of the climate-conditioned strategy vs static benchmark, 1985–2024. Source: Figure 3, Comolaet al. (2026).

Average returns were up to 30% higher, with the greatest gains at intermediate levels of risk aversion.

Compound annual growth rate was up to 35% higher for low-to-mid risk aversion profiles.

Risk-adjusted returns, measured by the ex-post Sharpe ratio, were up to 40% higher, reflecting improved returns alongside reduced volatility.

Average drawdowns in high-loss years were up to 50% lower, depending on risk aversion.

Year | Aggressive — Long-term | Aggressive — Seasonal | Conservative — Long-term | Conservative — Seasonal |

|---|---|---|---|---|

1992 | -10% | -25% | -11% | -8% |

2005 | -45% | -36% | -28% | -25% |

2012 | -7% | +1% | -1% | +2% |

2017 | -40% | -10% | -1% | +1% |

2022 | -10% | +0% | +3% | +4% |

Strategy returns in major loss years. Source: Table 1, Comola et al. (2026).

The preprint was posted to Research Square on 17 March 2026 and is currently undergoing peer review. Anonymized climate-conditioned loss tables and ILW premia used in the analysis are publicly available in a data repository.

In their words

"Working with the Reask team on this paper gave us a way to quantify something the ILS market has long debated: whether seasonal climate forecasts are actually actionable for portfolio decisions. The 40-year back-test suggests they are, and by a meaningful margin."

— Francesco Comola, LGT ILS Partners

Published sources

Comola, F., et al. Climate-Conditioned Catastrophe Modeling for Dynamic Risk Assessment, 17 March 2026, PREPRINT (Version 1) available at Research Square [https://doi.org/10.21203/rs.3.rs-9124834/v1]

Comola, F., & Bolliger, I. (2026). Climate-Conditioned Catastrophe Modeling for Dynamic Risk Assessment [Data set]. Zenodo. https://doi.org/10.5281/zenodo.19071628

Reask models used

The Unified Tropical Cyclone (UTC) model generates large ensembles of stochastic tropical cyclone seasons conditioned on meteorological and oceanographic forecasts, whether these are initial state-dependent seasonal forecasts (as in this study) or outputs of climate models looking at longer-term forced trends. UTC captures both the influence of the forced trends as well as year-to-year variability driven by the El Niño Southern Oscillation (ENSO), the Atlantic Meridional Mode (AMM), and other climate drivers.

CBRA (Climate-Based Risk Adjuster) is a Python package developed by Reask to adjust standard catastrophe model output to reflect a View of Risk conditioned to a desired climate state, such as that of an upcoming season.

Explore how the UTC model and CBRA can support seasonal risk forecasting and ILS portfolio optimisation. Chat to our team →

Stay in the loop

Sign up for the Reask newsletter for the latest climate science, model updates, and industry insights