The newsletter for climate-aware risk professionals.

The climate producing today's storms is not the climate that produced the historical record. Join 400+ risk professionals receiving the latest insights from Reask direct to their inbox.

Insights

How site-specific hazard data reduces premiums and basis risk in parametric insurance

Learn why loss-aligned parametric triggers like Metryc can reduce cost and uncertainty by aligning payout with actual location-level impact.

David Schmid

|

Global Head of Data Products

A parametric cover needs to pay when an event impacts the insured location. If we can deliver on that promise, there is no reason for parametric insurance to remain a niche product. This article explains why Reask's Metryc is one pathway to making that promise a reality.

Metryc, a loss-aligned parametric trigger, is a simple and intuitive solution for tropical cyclones, grounded in the core principles of (indemnity) catastrophe modelling:

Higher wind speed → higher losses → higher payout

This logical chain holds true at the location level. By contrast, the well-known Cat-in-a-Circle (CIC) operates at a macro level, which leads to:

1. High uncertainty in actual impact

For a Category 4 storm entering the circle, the actual wind speed at the covered location can vary by more than 100 km/h, ranging from tropical storm conditions to full Category 4 winds at the site.

2. Inflated premiums

All non-impacting events categorised as Category 4 are fully priced in, with the same weight as the rare cases where Category 4 winds actually reach the site. This means premiums are based on many stochastic events that cause little or no damage.

The outcome: higher cost.

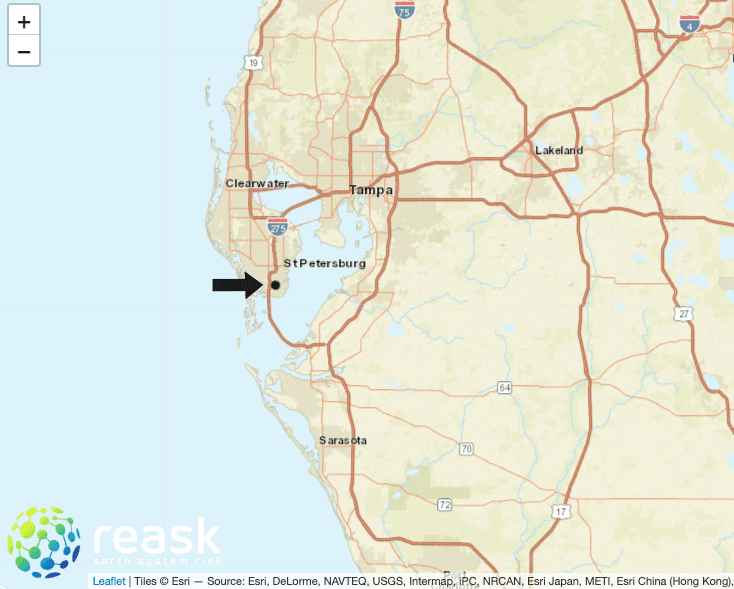

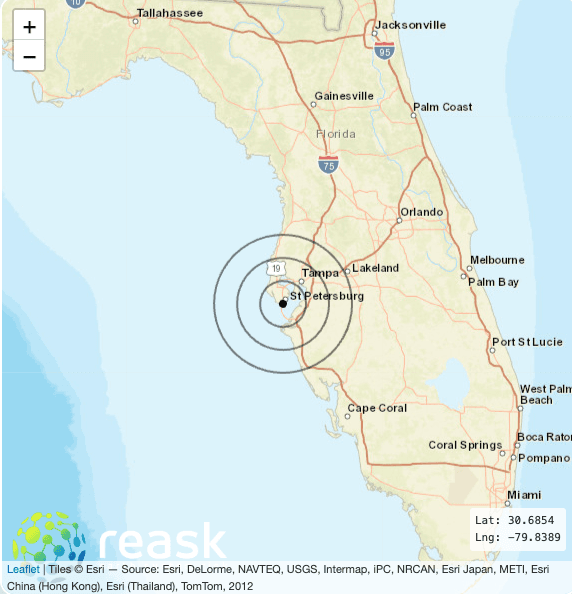

Theory is useful, but triggers are ultimately judged on real examples. So let’s look at one location in St. Petersburg, Florida, and compare Metryc with a CIC using two typical structures. Same risk, very different outcomes.

Probabilistic pricing

Metryc: 1 location

Metryc structure:

Windspeed | Payout |

|---|---|

100 kph | 5% |

120 kph | 15% |

140 kph | 40% |

160 kph | 70% |

180 kph | 100% |

Location limit: $10M

Cat in a circle (CIC): 1 location, 3 circles

CIC structure:

Cat 1 | Cat 2 | Cat 3 | Cat 4 | Cat 5 | |

|---|---|---|---|---|---|

25 km | - | 50% | 75% | 100% | 100% |

50 km | - | - | 50% | 75% | 100% |

75 km | - | - | - | 75% | 100% |

Location limit: $10M

Comparison:

Metryc: 2.3% expected loss (EL) – 10% standard deviation

CIC: 3.0% expected loss (EL) – 15% standard deviation

A Metryc cover is 22% less expensive on an expected payout basis.

Metryc also has a 33% lower standard deviation, reflecting lower volatility. CIC structures typically over- or underpay, and this uncertainty often drives higher premiums and capital allocation requirements.

Historical performance (1950–2024)

Metryc historical payouts since 1950:

Storm | Year | Payout |

|---|---|---|

Milton | 2024 | 7M |

Ian | 2022 | 1.5M |

Gladys | 1968 | 0.5M |

Alma | 1966 | 0.5M |

Easy | 1950 | 1.5M |

CIC historical payouts since 1950:

Storm | Year | Payout |

|---|---|---|

Milton | 2024 | 5M |

Comparison:

Metryc paid 5 times (1.5% historical rate)

CIC paid once (0.7% historical rate)

The CIC structure missed four events where the location was clearly impacted, not destroyed, but exposed to meaningful financial losses such as business interruption, non-damage BI, and clean-up costs. It paid for Milton, but not for Hurricane Ian.

Although Ian made landfall around 120 km to the south, it still caused power outages for over one-third of households in the wider St. Petersburg area and triggered widespread disruption, impacts that ultimately translate into real financial loss.

Interestingly, CICs are often marketed as a way to capture macro-economic impact. In this case, Metryc would have been the better choice not only for property damage, but also for non-damage business interruption.

Metryc is both less expensive and delivers lower basis risk at the same time, a combination that is rarely achieved in parametric insurance. This is the type of solution the market needs to unlock real growth, even in a soft market.

Want to see how Metryc prices for your locations? We can run a comparison against your current parametric structure in minutes. Request a demo →

Find out more about Metryc, including how it can be used as a double trigger alongside a CIC to unify the two approaches.